WebCab Portfolio (J2EE Edition)

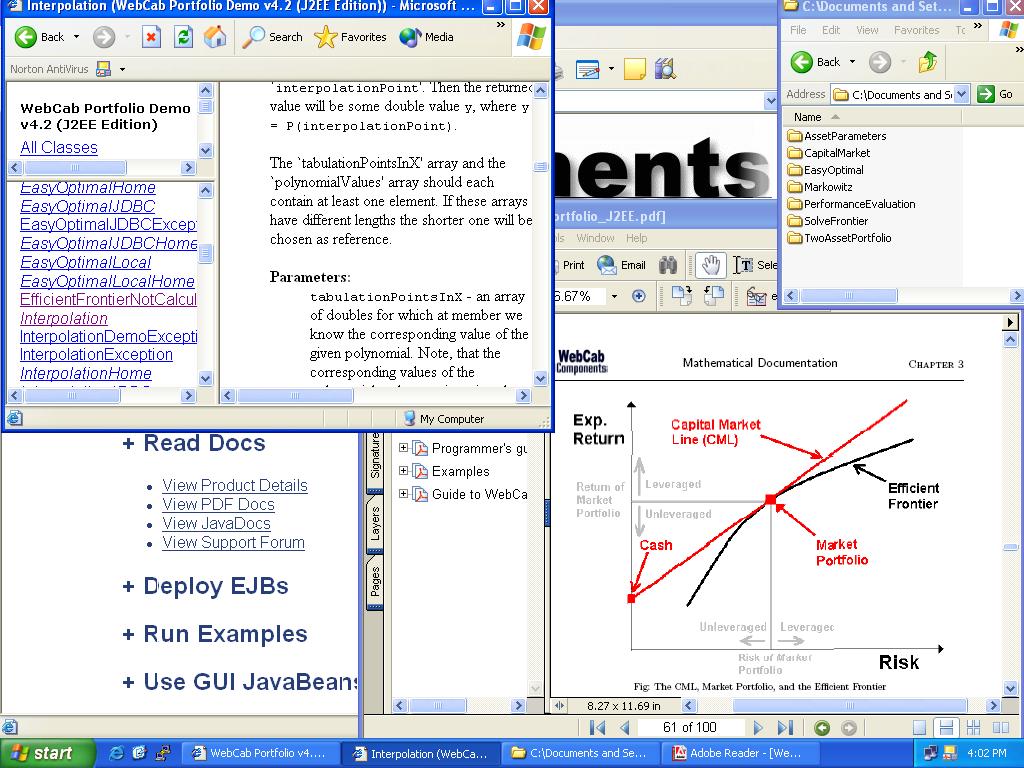

Apply the Markowitz Theory and Capital Asset Pricing Model (CAPM) to analyze and construct the optimal portfolio with/without asset weight constraints with respect to Markowitz Theory by giving the risk, return or investors utility function; or with respect to CAPM by given the risk, return or Market Portfolio weighting. Also includes Performance Evaluation, extensive auxiliary classes/methods including equation solve and interpolation procedures, analysis of Efficient Frontier, Market Portfolio and CML.